If nuclear is to matter meaningfully in India’s 2040 power mix, the country will now have to make up for decades of delay at almost breakneck speed

By Krishna V Giri & Payal Seth

The post–123 Agreement reality check

When India signed the Indo–US Civil Nuclear Agreement (aka 123 Agreement) in 2008, it was widely expected to unlock a new era of clean, reliable baseload energy. Access to global reactor designs and uranium fuel was supposed to accelerate nuclear capacity and reduce the country’s dependence on fossil fuels. Yet almost two decades later, nuclear power contributes barely 3% to India’s electricity generation, with total capacity at just 8.9 GW. This is roughly one-twentieth of France’s nuclear output (70% of electricity from nuclear power).

Since the signing of the Agreement, India has added ~2-3 GW of nuclear capacity, while solar power alone has grown by more than 110 GW in the same period. Structural frictions, such as land conflicts, safety concerns, local protests, financing hurdles, and lengthy construction timelines, have consistently undermined large reactor projects and left India with a nuclear program that has not matched its potential. If nuclear is to matter meaningfully in India’s 2040 power mix, the country will now have to make up for decades of delay at almost breakneck speed—compressing what should have happened over 30 years into the next 10–15.

The renewable expansion that masks deeper weaknesses

India’s renewable capacity now exceeds 235 GW, with solar accounting for over 123 GW. But generation data tells a more complex story. Solar output drops sharply during monsoon stretches. Evening peak demand arrives precisely when solar generation drops to zero. Storage remains prohibitively expensive, with round-the-clock renewable tariffs in the range of ₹8–10 per kWh. As a result, coal continues to generate roughly 70% of India’s electricity. Grid fragility remains visible in high-growth urban corridors like Chennai’s ECR region, where rain forecasts or heatwave-driven surges trigger preemptive shutdowns. Households and commercial clusters revert to diesel generators, pushing up pollution even as renewable capacity rises on paper.

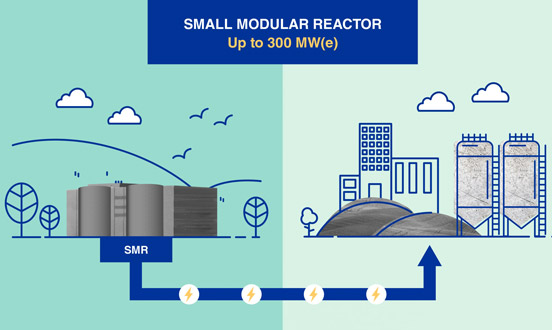

SMRs are advanced reactors that produce electricity of up to 300 MW(e) per module. (Photo courtesy: IAEA)

Why SMRs are emerging as the global middle path

Across many advanced economies, Small Modular Reactors (SMRs) are emerging as a serious option to complement intermittent renewables and avoid the long delays and cost overruns associated with large nuclear plants. The US Nuclear Regulatory Commission certified its first SMR design (NuScale) in 2023, with an updated design also approved in 2025. Canada is now targeting the first grid-scale SMR at Darlington to be online by around 2030 rather than 2028, with construction approvals and site works already underway.

The United Kingdom is running a national program to select SMR vendors, with Rolls-Royce recently chosen as the preferred bidder and other designs still in contention for future deployment. Countries such as Poland and Romania have also signed agreements with SMR developers as part of long-term plans to move away from coal and replace retiring thermal plants. These efforts reflect a wider global understanding that deep decarbonization is difficult to achieve with renewables alone without very large storage or backup capacity. SMRs are therefore attracting interest as a potential source of reliable, low-carbon, dispatchable power.

India’s challenges mirror those driving this global interest. Large nuclear parks (from Jaitapur in Maharashtra to multi-unit expansions at Kudankulam in Tamil Nadu) have faced delays resulting from land issues, public opposition, construction hurdles, and complex regulatory processes. Financing a single 1,650-MW reactor remains a significant sovereign and commercial undertaking.

SMRs, by contrast, require far less land and use passive safety systems, and their modular construction is intended to shorten build times once manufacturing scales up. If these efficiencies materialize, SMRs could offer India a cleaner and potentially faster route to adding firm power capacity than traditional large reactors.

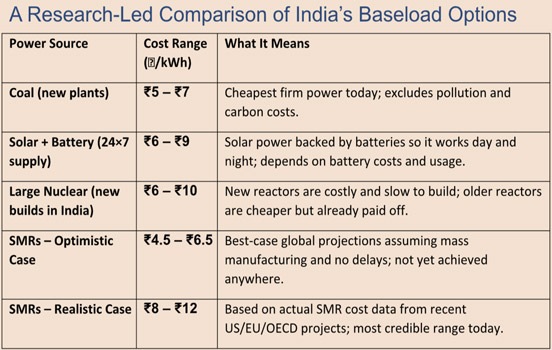

(Table courtesy of the authors)

To compare different electricity sources, analysts use the Levelized Cost of Electricity (LCOE) — the average cost of producing one unit of power over a plant’s entire life. Coal remains cheap but polluting. Solar becomes expensive when combined with batteries for a 24×7 supply. Large nuclear plants can be economical over time, but take a decade or more to build. SMRs are promising, but current real-world costs are still high. Their lower projected costs are based on future manufacturing scale that has not yet materialized.

This comparison shows why India needs a mix: renewables for daytime, and reliable, clean sources like nuclear (especially SMRs in the long term) to cover evening peaks, monsoon variability, and industrial demand.

Governance, not technology, is the binding constraint

The economics of SMRs are promising in theory, but India’s institutional architecture remains the limiting factor. The nuclear sector is still dominated by the state under laws drafted in the 1960s (notably the Atomic Energy Act, 1962), and private participation in nuclear generation is heavily restricted to minority or vendor roles. This limits manufacturing scale, innovation, and capital mobilization. Power Purchase Agreements (PPAs), typically 20–25 years in tenure for large projects, often fail to pass generation cost reductions to consumers in a timely way.

A modern grid cannot run on mid-20th-century governance frameworks. India will need legal reforms that allow domestic private firms to co-develop and eventually operate SMRs under transparent regulatory oversight. A new class of performance-linked PPAs for firm clean power will also be essential. Equally important will be policy instruments that actively reward private risk-taking: building on Production-Linked Incentive (PLI) schemes and extending them into innovation-linked or risk-sharing frameworks for nuclear components, fuel-cycle services and SMR project development, so that private players have a clear upside for coming in early rather than waiting on the sidelines.

Choosing the energy architecture of the next two decades

By 2040, India is expected to account for the largest share of global growth in overall energy demand, adding consumption comparable to that of a major advanced economy such as the European Union. Historically, most industrialized countries that have deeply decarbonized their power sectors have relied on substantial contributions from nuclear, large hydro, or both as part of a diversified, firm, low-carbon mix. India, however, does not need to replicate the legacy model of vast, centralized nuclear parks. It has the opportunity to leapfrog toward a distributed, modular, nuclear (renewable hybrid system), one in which solar and wind dominate daytime supply, while SMRs eventually provide clean, firm power during evenings, monsoons, heatwaves, and industrial peaks.

Such a shift could significantly reduce reliance on diesel generators and gradually push coal into a legacy role rather than an enduring dependency. But this will only happen if India moves at near breakneck speed on three fronts simultaneously: reforming nuclear law, inviting full-scale domestic and overseas private participation, and putting serious incentive money—PLI-style, innovation-linked and risk-sharing—behind SMRs and the broader clean-firm power ecosystem. Whether India seizes this opportunity will shape not only the reliability of its power sector but the competitiveness of its economy in a climate-constrained world.

(Krishna V Giri is a Distinguished Fellow & Special Advisor to the Chairperson, and Payal Seth is a Fellow. Both are at Pahle India Foundation, a New Delhi-based think-tank)