By Vivek Jain

Apart from equities, NRIs can also explore insurance-cum-investment products that help with wealth creation.

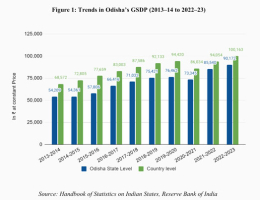

India is one of the fastest-growing economies in the world, expected to become the third-largest by 2027 as per the Finance Ministry. Blessed with a young demographic, India is going through a phase of digital transformation and policy reforms. This has made it a magnet for both foreign capital and the savings of NRIs.

For millions of Non-Resident Indians (NRIs) living across the world, India remains a second home. They have emotional and family ties in India. But that is not the only reason they stay connected. It is also about making smart choices and tapping into India’s strong economic growth potential. Being an NRI gives them a unique advantage to leverage their connection to grow their personal wealth as India’s economy booms.

While the opportunity is exciting, navigating insurance and investment regulations can feel complex. This is especially true if you’re sitting thousands of miles away in a distant land. So let us break down the key insurance products to consider, and the investment avenues to grow your wealth. Whether your goal is to protect your family, create a retirement cushion, or simply stay connected to India’s economic momentum, here’s what you need to know.

Why insurance from India should be on your radar

While it’s important to focus on wealth creation, overlooking protection is not the mistake you should be making. A sudden illness, accident, or untimely death can create not only emotional distress but also severe financial setbacks for loved ones in India. And that makes insurance extremely crucial.

First and foremost, one must consider a term insurance plan from India. This plan provides a lump-sum payout to your family if something happens to you. In India, term plans are a lot cheaper than in developed countries like the US. If one has financial liabilities and dependents in India, consider a high-sum assured term plan of at least Rs 2 crores.

Term plans for NRIs are created for the distinct needs of Indians staying overseas. Features like special exit for a full refund of the premium, claim intimation benefits, health management services, or early payout for terminal illness add to the policy value.

Second, buying a comprehensive health insurance plan from India makes a lot of sense for NRIs. Medical care is a lot cheaper in India compared to the US. Many NRIs plan their non-urgent medical treatments in India. And while this is more affordable compared to the US, medical inflation does run in double digits in India. A health insurance plan helps. After all, a hospital stay or long-term treatment can quickly erode your savings.

NRIs should also consider buying a comprehensive health plan for their senior citizen parents in India. Many insurers now offer specialized senior citizen plans with cashless treatment at top hospitals. There is even on-ground support available to guide them through the process, even in your absence. If you have a family history of cancer, heart disease, or similar conditions, adding a critical illness rider or standalone policy can cover expensive treatments. NRIs are also eligible for an 18% GST refund on both their health and term insurance premiums paid via NRE (non-resident external) bank accounts.

Exploring investment opportunities in India

Along with fulfilling your protection needs, NRIs can start exploring investments. Apart from equities, they can also explore insurance-cum-investment products that help with wealth creation.

If we talk about market-linked insurance plans known as ULIPs, they combine the discipline of insurance protection along with the growth potential of market-linked returns. This makes them especially useful for NRIs who want to create wealth over the long term while safeguarding their family’s financial future. Most traditional investments only do one job. They either grow your wealth or protect it.

ULIPs are designed to do both. When you buy a ULIP, a portion of your premium is invested in market-linked funds, such as equity, debt, or balanced funds, depending on your choice, and the rest of the portion helps provide financial security for your family in case of an untimely demise. This makes ULIPs a powerful tool to build a corpus for long-term goals like children’s education or retirement.

One must note that ULIPs are not designed for quick exits. In fact, they come with a mandatory lock-in period of five years, which helps investors stay committed to long-term wealth creation. This disciplined approach aligns perfectly with NRI goals like accumulating wealth and planning for a future return to India. Equity-oriented ULIP funds have the potential to deliver inflation-beating returns over a 10–15-year horizon, while debt or balanced funds offer stability. One can also choose a mix of both, or even switch between them seamlessly, depending on their stage of life or the prevalent market situation.

Finally, NRIs can also consider fixed income instruments like guaranteed return plans, which can offer predictable cash flow in this unpredictable world. For example, if you put Rs 30,000 monthly for 5 years, and withdraw after 10 years, your invested value of approximately Rs 18 lakh would be close to Rs 29 lakh at the time of maturity. This will be regardless of market fluctuations or currency rates. These plans are “set and forget” investments and require no active monitoring once you have invested. Plus, these plans also offer a life insurance component, which makes them useful for NRIs who want both protection and guaranteed accumulation.

India’s economy is growing at a rapid pace. Infrastructure investments are creating new economic corridors. Digital adoption has transformed how Indians buy, bank, and invest. For NRIs, this is more than just a sentimental pull. It is also a way to participate in the country’s remarkable growth while building personal wealth.

.jpg)

(The writer is Chief Business Officer, Life Insurance, at Policybazaar.com)